October is Cybersecurity Awareness Month — a great time to pause and reflect on how much our daily lives now depend on digital tools: smartphones, computers, online banking, telehealth, email, and social media. But with all that convenience comes risk. The good news is that with a few simple habits, most people can make life online a lot safer. Here’s a simple guide to what the cyber world looks like now and how to protect yourself

The Cyber Landscape Today: Why It Matters

The internet is more powerful than ever — but so are the tools that criminals use to exploit it. Here are some headline stats:

Cybercrime damages are projected to reach $10.5 trillion per year globally by 2025.

In 2025, credential theft (stealing usernames and passwords) surged by 160% over prior periods.

Among older adults (60+), the FBI reports that $6 billion was lost to digital scams in 2024 alone; 41% of seniors who lost $10,000 or more experienced scams that began with a phone call. These numbers may seem overwhelming, but they highlight why vigilance is so important

What Makes Certain People More Susceptible

Some people face special challenges in the digital realm:

Trusting communications. Scammers sometimes pose as banks, the IRS, or grandkids in need — and it can be emotionally compelling.

Legacy devices. Many people keep older computers, phones, or tablets longer. Those often don’t get updates or security patches.

Using many services. From Medicare portals to online banking and shopping, there are multiple points of vulnerability.

But none of this means you’re helpless. Let’s look at what you can do

Simple Practical Protections You Can Us

These steps don’t require you to be a tech wizard — just a little care and consistency.

Area

What You Should Do

Why It Help

Passwords

Use strong, unique passwords for each account (a mix of letters, numbers, and symbols). Using a password manager can help store and generate unique passwords, so you only need to remember one “master” password.

A compromise of one account doesn’t lead to a domino effect.

Multifactor

Enable Multi-Factor Authentication (MFA) (e.g., text message code, authenticator app).

Even if someone gets your password, they can’t log in without the second factor.

Software & Device

Turn on automatic updates (for your operating system, apps, and browser).

Use antivirus/anti-malware software and keep it up to date.

Many attacks exploit known vulnerabilities in outdated software.

It helps catch threats before they cause damage.

Email & Links

Don’t click links or attachments in suspicious or unexpected emails or texts.

If a message claims an urgent issue (bank, government), don’t respond directly. Instead, open a browser and go to the official site (or call using a known number).

Many attacks begin with phishing (fake emails or spoofed sources).

Scammers often try to rush you into mistakes.

Web & Shopping

Use websites that show “https://” and a padlock icon (meaning secure), especially for anything involving money or personal data.

Avoid entering account passwords on public Wi-Fi networks (coffee shops, libraries).

Encryption helps prevent eavesdroppers from intercepting data.

Public Wi-Fi is easier to exploit.

Social Media & Sharing

Think twice before posting personal info (birthday, address, phone), especially in public profiles.

Adjust privacy settings so only “friends” (people you know) see your full profile.

That kind of information can help scammers impersonate or socially engineer you.

Minimizes exposure to strangers.

Financial Precautions

Use credit cards (rather than debit) for online purchases — they often have better fraud protection.

Monitor your bank statements and set up alerts for unusual activity (withdrawals, large transfers.

Be extra cautious about wire transfers or giving money to someone you don’t know, especially if someone is asking you to pay in bitcoin. Scammers like using bitcoin because it’s harder to track them down.

Banks tend to give stronger consumer protections on credit lines.

Early detection is your best defense.

Scam artists often pressure people to send money “fast.”

When in Doubt

Ask a trusted, tech-savvy friend or family member to look things over before you take big actions online. If you feel something is wrong, disconnect from the internet and seek help — don’t ignore it. Don’t be embarrassed to ask for help; it could save you in the end. Sometimes a second pair of eyes spots red flags. The sooner you act, the less damage is possible.

A Final Word

Cybersecurity isn’t about perfection — it’s about layers of protection and awareness. Even simple steps can make a huge difference. As crimes become more sophisticated, the most basic defenses (strong passwords, updates, cautious clicking) become even more essential. Especially if you’re retired or not deeply into tech, these practices can help protect your savings, identity, medical records, and peace of mind

Our employee Elayne Pisarik says “Success comes when your finances do not define your happiness. A full life – whether defined by family or other relationships, faith, employment or a combination of all of those – that comes without concern or worry about money is a powerful thing.”

After years of work and preparation, your first month of retirement isn’t just a change in schedule — it’s the foundation for your new lifestyle. The choices you make in these early weeks can shape your long-term financial confidence, emotional balance, and sense of purpose.

At Firstrust, we often tell clients: retirement isn’t an ending — it’s a transition. Here’s how to use your first month wisely.

1. Revisit Your Budget with a New Lens

Your cash flow looks different now. Instead of a paycheck, you’ll draw income from savings, investments, and possibly Social Security or pensions.

Review your expected monthly income versus expenses.

Track your spending patterns for at least the first 30 days.

Adjust as needed — it’s a learning curve, not a test.

A clear budget helps you spend confidently without second-guessing your decisions.

2. Create a Healthy Daily Rhythm

Your first month should balance rest, structure, and well-being.

Many new retirees feel pressure to fill their schedules immediately, but it’s perfectly fine to slow down. Start with a simple daily rhythm — morning walks, time with friends, or a relaxed hobby. Physical movement, social connection, and quiet reflection all support mental and physical health.

Think of it as designing the pace of your new life — one that energizes you without overwhelming you.

3. Retirement is a major achievement — acknowledge it.

Whether it’s a family gathering, a long-awaited trip, or a quiet dinner with loved ones, celebrating helps mark the transition and create a sense of closure from your working years.

4. Define What’s Next

Without the structure of work, it’s important to define what fulfillment looks like now. Ask yourself:

What do I want to learn or experience?

How do I want to contribute — through mentoring, volunteering, or creative pursuits?

What kind of legacy do I want to leave?

Your answers will guide how you invest your time and energy in the years ahead.

5. Meet with Your Financial Advisor Early

Your finances are the foundation of your freedom in retirement. Schedule a review with your FirsTrust FinancialTeam to discuss:

Sustainable withdrawal strategies

Tax-efficient income planning

Investment allocation for income and growth

Contingency planning for unexpected needs

The sooner you align your financial plan with your new lifestyle, the more confidently you can enjoy it.

The FirsTrust FinancialTeam Perspective

The first month of retirement is about clarity, not perfection. By intentionally setting your financial and personal rhythm early, you build the foundation for a fulfilling, sustainable retirement.

At FirsTrust, we help clients transition from accumulation to enjoyment — guiding every step with structure, care, and long-term confidence.

As Seen in WSJ | Buy Side Dated 8/19/2025 Written By Molly Grace

Explore the different categories of financial advisors—from RIAs to robo advisors—to determine which expert aligns with your financial planning needs

Key takeaways

There are many different types of financial advisors. The right one for you will depend on your unique financial needs.

Financial advisors can offer comprehensive financial planning, investment advice, hands-off automated investing or some combination of all of these services.

As you search for a financial advisor, consider how they’re paid, whether they’re a fiduciary and if they offer the services you’re looking for.

There are a lot of different terms used to describe financial professionals, which can make it hard to know which one is right for you. But you can make your search easier by knowing what types of services you’re looking for.

What are fee-only financial advisors?

There are three main ways that financial advisors earn money:

Fee-only: Financial advisors who are fee-only are solely paid by their clients and don’t earn commissions selling financial products.

Fee-based: With this pay structure, advisors are paid by their clients, but they can also earn commissions selling financial products like insurance to their clients.

Commission-based: Some financial advisors are only paid through the commissions they earn selling financial products to clients.

Bridget Grimes, a certified financial planner and president of WealthChoice, says the way an advisor is paid can potentially present a conflict of interest. If an advisor relies only on commissions, they might recommend products to you that aren’t necessarily in your best interest.

Fee-only advisors, she says, don’t have that same conflict of interest.

“That person who’s going to give you guidance is going to be agnostic when it comes to investments,” Grimes says.

It’s common for advisors to charge a fee based on a percentage of the assets they manage for you, but you might also come across advisors who charge hourly fees, flat fees or retainers.

Fiduciary financial advisors

Advisors who are held to a fiduciary standard are obligated to make recommendations that are in their clients’ best interests. Not all financial advisors are held to this standard.

“There are two different standards in the industry, there’s a suitability standard and a fiduciary standard,” says Kathryn Berkenpas, a certified financial planner and managing director of corporate growth at CFP Board. “Suitability means you have to meet the requirement that it is suitable for the client. But that doesn’t mean it’s absolutely in the client’s best interest.”

Fee-only financial advisors typically operate under a fiduciary standard, while advisors who earn commissions might only be held to a suitability standard.

Certified financial planners (CFPs) are held to a fiduciary standard by the CFP Board, the organization that offers the CFP certification. Registered investment advisers (RIAs) are required by law to act as fiduciaries.

What are robo advisors?

Robo advisors use technology to create investment portfolios for users. They automate the investing process and make it easy for beginners to start investing. Robo advisors can be used for both general investing and retirement saving.

“We typically see robo advisors used for a retirement plan,” Berkenpas says. “So [robo advisors are used] to give an asset allocation for a pot of money, to grow that pot of money to be the right size at the right time.” But they’re limited in how much they can help you with your overall financial plan.

When you open an account with a robo advisor, you’ll typically answer some questions about your financial situation, retirement plans and risk tolerance to help the algorithm build a portfolio that suits your needs. Then it will automatically manage your funds, rebalancing your portfolio as needed.

Robo advisors often have lower account minimums and advisory fees compared to traditional advisors, which is why they can be a good choice for new investors. You might want to work with a financial advisor instead of a robo advisor if you have more complex financial needs or a larger portfolio.

What are broker-dealer advisors?

Broker-dealers are financial professionals or institutions that buy and sell securities for their own accounts and on behalf of their customers.

“A broker-dealer is a wirehouse,” Grimes says. “These are, for example, Morgan Stanley and UBS. They’re traditionally seen as more investment-forward. When I worked at a broker-dealer, they were investment-forward. We did not do financial planning.”

Broker-dealers vs. RIAs

Broker-dealers buy and sell investments on behalf of their clients and generally earn a commission on those transactions. RIAs focus more on managing their clients’ portfolios and giving them investment advice. RIAs typically earn money through fees paid by the client.

However, there’s more overlap between broker-dealers and RIAs now than there used to be, Berkenpas says. Many firms now offer both types of services.

What are hybrid advisors?

Individuals or firms that offer both brokerage services and investment advising services are known as hybrid advisors. A hybrid advisor might earn both commissions on investment transactions and charge a fee based on the assets they manage for you.

“It used to be that they had different compensation structures and legal structures, and some followed the suitability standard, and some followed the fiduciary standard,” Berkenpas says. “A broker-dealer can be a hybrid now and also work as an RIA.”

Because they’re RIAs, hybrid advisors are held to a fiduciary standard, so they have to recommend financial products that are the best fit for your situation.

Hybrid robo advisors

You might also see the term hybrid advisor used to refer to a type of robo advisor service that includes access to a financial advisor. Hybrid robo advisors can be a good middle ground between a completely hands-off automated investment strategy and comprehensive planning offered by an investment advisor or financial planner. But some robo advisors require higher account minimums or charge higher fees to have access to a financial advisor.

How advisor services vary by specialization

Financial advisors can offer a wide range of services, but both Berkenpas and Grimes warn that relying on the terms advisors use to describe themselves isn’t always the best way to get a sense of what those professionals offer.

“You can’t choose the best professional for what a consumer is looking for based on compensation, job title or strictly if they’re at a broker-dealer or if they’re an RIA,” Berkenpas says. “It’s really about finding out what the professional does and what you need as a consumer.”

Grimes says that, as you interview potential advisors, you should ask questions about what services the person offers so you can understand “whatever they’re calling themselves, are they able to provide the guidance that you’re looking for?”

Who should consider each type of financial advisor?

To find the right type of financial advisor for you, think about what you need. If you’re looking for comprehensive portfolio management or financial advice, an RIA or CFP may be a better choice than a robo advisor, for example. In this case, you might also want to prioritize working with a professional who’s held to a fiduciary standard, or someone who doesn’t earn any commissions.

But if you’re early in your career and want to start putting away money for retirement, having a portfolio with a robo advisor might be all you need.

If you’re considering working with a financial advisor, interview a few different candidates to find out what types of services they offer, how they’re paid and what types of clients they work with, Grimes says.

“Are they familiar with people like you and the challenges you have?” she says. “If you’re working with somebody who has a totally different life experience, I’m not so sure that that’s the best person to guide you.”

FAQ

What is the difference between a fiduciary and non‑fiduciary advisor?

A fiduciary advisor is legally obligated to act in their client’s best interest—regardless of whether it financially benefits them—and disclose any conflicts of interest. A non-fiduciary advisor is not bound by the same legal standards as a fiduciary financial advisor. They are obligated to make suitable recommendations for their clients and might earn a commission from the investment products that they sell.

Do robo advisors work for high-net-worth clients?

Robo advisors, which offer automated portfolio rebalancing, could be a convenient option for clients in need of a more hands-off approach. Traditional financial advisors might make more sense for high-net-worth individuals who have complex financial needs and are looking for customizable, comprehensive portfolio options. Some robo advisors also offer a hybrid option where you can consult with a financial advisor, which might provide a happy medium.

Can I switch between advisor types over time?

Yes, you can switch between a robo advisor and a human advisor if your needs change over time. You can also opt for a hybrid advisor, which combines the cost-effective and convenient aspect of a robo advisor with the hands-on, personalized advice that a traditional financial advisor offers.

Are hybrid advisors more expensive than robo advisors?

Hybrid advisors are typically more expensive than robo advisors but more affordable than traditional advisors. It’s common for hybrid advisors to charge between 0.30% and 0.65%. Robo advisors charge a median annual fee of 0.25% of assets under management (AUM), according to the most recent Morningstar robo advisor report, and traditional advisors charge 1.05% AUM on average, according to a 2024 Envestnet advisor survey.

How do financial planner credentials differ across advisor types?

There are many different credentials that financial advisors can have, though they aren’t necessarily confined to specific types of advisors. Around 1 in 3 financial advisors are CFPs, according to the CFP Board. As advisors, CFPs can offer holistic financial planning or have a more specific focus like investment management. Chartered financial consultants (ChFCs) also receive financial planning training and might create comprehensive plans for clients. An advisor who focuses more on investing might also have a chartered financial analyst (CFA) credential, while an advisor with an accredited financial counselor (AFC) certification might focus more on helping clients with budgeting and debt reduction. Retirement income certified professionals (RICPs) cater to clients planning for retirement.

Estate planning isn’t just a one-and-done task; it should evolve with your life, family, and the law. If your revocable living trust was created before 2011, chances are it’s no longer optimized for today’s tax laws or family dynamics. Laws have shifted dramatically, especially with the introduction of portability, making older A-B Trusts potentially obsolete and even harmful.

An outdated trust could burden your family with extra taxes, administrative headaches, and restricted access to inherited wealth. This article explores what’s changed, why it matters, and what steps you should take now.

What Is a Revocable Living Trust?

A revocable living trust is a legal document that lets you control your assets during your lifetime and specify how they should be distributed after death – all without going through probate. You can alter, amend, or revoke the trust at any time while you’re alive.

Key Advantages for Families

Avoids probate, saving time and money

Keeps your affairs private

Allows you to name trustees and successors

Provides flexibility in managing incapacity

Helps in multi-state property management

The Rise and Fall of Revocable Trusts with A-B Provisions

What Is an A-B Trust Structure?

An A-B Trust splits into two parts to capture both spouses’ exemptions after the first spouse dies:

The A Trust (Marital Trust): Holds the surviving spouse’s share.

The B Trust (Credit Shelter Trust): Contains the deceased spouse’s exempt assets.

Why They Were Essential Before 2011

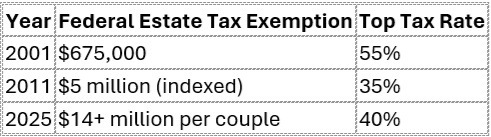

Before 2011, the estate tax exemption wasn’t portable. If unused upon the first death, it was lost. To retain it, couples had to use A-B Trusts to “lock in” the deceased spouse’s exemption.

How Tax Law Changes Made A-B Trusts Obsolete

Thanks to the 2010 Tax Relief Act and later permanent adoption in 2013, the IRS allowed portability of the estate tax exemption between spouses. That means the surviving spouse can inherit any unused portion of the deceased spouse’s exemption via the DSUE (Deceased Spouse Unused Exemption).

A-B Trusts are now unnecessary for most Americans due to today’s $28M+ combined exemption for married couples.

Consequences of an Outdated Revocable Living Trust

Loss of Second Step-Up in Basis

Assets held in a Credit Shelter Trust don’t receive a second step-up in basis upon the surviving spouse’s death. That means your children could face large capital gains taxes when they sell inherited assets.

Restricted Spousal Access to Trust Assets

Even if the surviving spouse is the trustee, access to B Trust assets is often limited to HEMS (Health, Education, Maintenance, Support) standards. In contrast, a modern trust allows full access and control while still preserving the exemption.

Increased Administrative Duties

Credit Shelter Trusts come with burdensome legal responsibilities:

Without a basis adjustment, appreciated assets in the B Trust result in a taxable gain upon liquidation. That means less inheritance for your beneficiaries.

Key Legal Responsibilities for Florida Trustees

Compliance and Fiduciary Duties

Florida trustees must:

Separate personal and trust assets

Maintain accurate records

Act in good faith and in the best interest of all beneficiaries

IRS Reporting Requirements

IRS Form 1041 must be filed annually if trust income exceeds $600.

Strict accounting rules apply to ensure transparency and proper distributions.

Warning Signs Your Trust May Be Outdated

Created or last reviewed before 2011

Includes automatic Credit Shelter Trust funding

Lacks portability or DSUE references

Surviving spouse has limited access to trust assets

You never filed Form 706 after your spouse’s death

Inflexible terms for blended families

Heirs face capital gains tax on inherited assets

If any of these apply, it’s time for an urgent review.

Modern Alternatives to Outdated Trust Structures

Portability-Friendly Trust Design

Today’s trusts can preserve both tax exemptions without dividing assets unnecessarily. This simplifies management and preserves tax efficiency.

Customization for Blended Families

New planning techniques include:

QTIP trusts for second spouses

Lifetime beneficiary protections

Conditional distributions based on remarriage or blended heirs

Tax-Efficient Planning Tools

Disclaimer Trusts offer flexibility

SLATs (Spousal Lifetime Access Trusts) and IDGTs (Intentionally Defective Grantor Trusts) for large estates

Filing Form 706 to elect portability—even late, with IRS approval

FAQs: Is Your Revocable Living Trust Outdated?

Do I still need an A-B Trust in 2025? Only if your estate is well over $14 million. Most families can now rely on portability instead.

What is a step-up in basis, and why does it matter? It adjusts the value of inherited property to its market value at death, minimizing capital gains tax when sold.

What is the DSUE amount? It’s the Deceased Spouse’s Unused Exemption—a portable estate tax exemption transferred to the surviving spouse.

Can I fix an outdated trust without starting over? Yes. You can amend or fully restate your trust depending on its condition and the needed changes.

What happens if I never filed Form 706? You may still be eligible for a late portability election—consult with a tax attorney immediately.

What are HEMS standards? HEMS stands for Health, Education, Maintenance, and Support, often used to restrict distributions to beneficiaries.

Conclusion: Don’t Let an Old Trust Hurt Your Legacy

If your revocable living trust hasn’t been updated in over a decade, it could be doing more harm than good. Outdated A-B Trust structures, once essential, are now often counterproductive due to changes in tax law. The good news? With help from a qualified estate planning attorney, you can modernize your plan, reduce taxes, and simplify your family’s financial future.

Take the time now to review and update your trust. Your heirs will thank you.

About the Author

Michael T. Koenig, CFP®, J.M., is the Founding Partner of FirsTrust, LLC. With over 35 years of experience as a professional financial advisor, Michael candidly shares his insights to promote truth and transparency for financial service consumers. He holds a bachelor’s degree in psychology from the University of Maryland, a master’s certificate in finance from George Washington University, a Juris Master of Law degree from Florida State University College of Law, and the CFP® Certified Financial Planner™ designation.

At FirsTrust, clients are served by a FinancialTeam of experienced financial specialists who have sworn a fiduciary oath to preserve their objectivity by refusing to accept the industry’s typical kick-backs and marketing incentives.

Cal 1-800-585-9888 to request a free review of your estate plan. We aren’t lawyers, insurance salesmen or commission-paid financial planners: no cost and no sales pitch.

A great financial advisor is worth their weight in gold, especially when you’re planning for retirement. Not every advisor specializes in retirement planning, so it helps to know how to identify someone who truly understands the unique tradeoffs retirees face: income planning, required minimum distributions, Social Security timing, and longevity risk.

Here, we cover how you can know you’re working with someone who will put your needs and goals above all else as you plan for retirement.

As you read this, give yourself two big pats on the back: One for putting in the work to earn your college degree and one for finding this article. The fact that you’re here shows you’ve already taken the most important step toward financial freedom by starting your investment education.

Often, the biggest hurdle to investing is simply a lack of knowledge. The prospect of learning how to invest can feel so overwhelming that many put off starting altogether. But the good news is that investing doesn’t need to be complicated, nor do you need to study for it as if there will be a final test. All you need to do to start investing is to start investing. That said, just diving in with no preparation can lead to some potentially costly blunders.

And while you likely have enough time on your side to recover from any near-term mishaps, a bit of advice beforehand can pay off in the long run. So here is the best investing advice for college grads, according to financial experts.

In theory, a client who receives full disclosure about a conflict of interest would not knowingly consent to an action that would clearly harm them. The core premise of “informed consent” is that the client understands both the conflict and its potential impact on them.

However, several factors complicate this in practice:

Information asymmetry

– Clients often lack the expertise to fully evaluate the implications of what they’re consenting to, even with disclosure. They rely on the adviser’s expertise, which is why they sought professional help in the first place.

Disclosure framing

– How conflicts are disclosed matters tremendously. Research has shown that disclosures can be presented in ways that minimize perceived risks or normalize conflicts.

Trust dynamics

– Many clients have strong trust in their advisers and may consent primarily based on that trust rather than critical evaluation of the disclosed conflict.

Hidden or indirect harms

– Some conflicts lead to suboptimal outcomes rather than direct harm (like slightly higher fees or marginally lower returns), making the harm less obvious during the consent process.

Psychological factors

– Clients may rationalize accepting conflicts due to status quo bias, wishful thinking, or to avoid the hassle of finding a new adviser.

This is why many regulatory approaches recognize that disclosure alone is insufficient protection, and why some conflicts are prohibited outright regardless of disclosure and consent.

The ideal fiduciary framework requires both informed consent AND that the action remains in the client’s best interest despite the conflict – not merely that the client agreed to it.

The Substantive Fairness Test

To test the validity of the informed consent, and/or to ensure the client’s best interest remain paramount, the courts have traditionally applied the

substantive fairness test. This requires that, even with disclosure and consent, the transaction must be objectively fair to the client. This means:

The terms of the transaction must be at least as favorable to the client as those the client could obtain in an arm’s-length transaction with an unrelated third party.

The fiduciary cannot take advantage of their position to benefit themselves at the client’s expense.

The transaction must provide a genuine benefit to the client or at minimum, not harm the client’s interests.

Substantive fairness is a legal concept that goes beyond procedural fairness, examining the fundamental equity and reasonableness of a transaction or decision itself. It asks whether the substance of an agreement is just, balanced, and protective of the interests of the potentially disadvantaged party.

The Key Aspects of Substantive Fairness include:

Intrinsic Reasonableness

Evaluates the actual terms and outcomes of an agreement

Ensures the substance of the deal is fundamentally equitable

Looks beyond mere technical compliance to assess genuine economic and practical fairness

Economic Equivalence

Determines whether the transaction provides comparable value to all parties

Checks if the terms are comparable to what would be achieved in an arm’s-length market transaction

Prevents exploitation through technically legal but economically predatory arrangements\

Protection of Vulnerable Parties

Provides special scrutiny when power imbalances exist

Prevents stronger parties from leveraging their position unfairly

Contextual Analysis

Considers the specific circumstances surrounding the transaction

Evaluates fairness not through abstract standards, but through the lens of practical, real-world implications

On the Application of the Requirements of “Informed Consent” and “Substantive Fairness” to Investment Advisers

The U.S. Securities and Exchange Commission has long adopted the requirement of

informed consent. This differs from mere consent. While beyond the discussion of this article, mere consent in an arms-length relationship can lead to waiver and/or estoppel. However, in a fiduciary-client relationship the application of waiver and/or estoppel is very limited.

The U.S. Securities and Exchange Commission has not expressly incorporated the “substantive fairness test” into its rulemakings on the fiduciary standard. It has, however, stressed that remaining conflicts of interest must be “properly managed.”

In some fiduciary-entrustor relationships, such as attorney-client, or trustee-beneficiary, procedures exist (such as judicial review and approval) that protect the entrustor (the client, or beneficiary). But such protection does not exist in the investment adviser-client context.

The difficulty with managing conflicts of interest in financial services is that most of them arise from compensation structures. For example, the investment adviser (or her/his firm) receives greater compensation when undertaking one recommendation, versus another. This may occur due to receipt of soft dollar compensation, 12b-1 fees, marketing support payments, other forms of revenue sharing, or simply by achieving better economies of scale that support the profitability of a proprietary mutual fund or other investment product.

In essence, when greater compensation is received by an investment adviser, resulting from a specific product recommendation, the client usually incurs greater fees and/or costs. And the academic evidence is robust and clear – the greater the fees and costs, then (on average) the lower the returns to the client, all other things being equal.

The No-Conflict and No-Profit Rules: Why Conflicts of Interest Should Be Avoided

One can conclude that, given the inherent difficulty of “properly managing” conflicts of interest – so that the client is never harmed (relative to an alternative course of action that could have been recommended), and instead the client always receives the benefit of truly expert, objective (trusted) advice – most conflicts of interest must be avoided by investment advisers.

The

“no-conflict rule” and the “no-profit rule” are core components of the fiduciary duty of loyalty. These rules fined their roots in the precept – derived from biblical principles and since uttered by many a jurist – that “no man can serve two masters.”

About the No Conflict Rule (Duty of Loyalty):

Prohibits a fiduciary from placing themselves in a position where their personal interests conflict with their client’s interests

Requires the fiduciary to avoid situations that might compromise their ability to act solely in the client’s best interest

Applies even to potential or prospective conflicts, not just actual conflicts

Mandates absolute priority of the client’s interests over the fiduciary’s own

Extends to both direct and indirect conflicts of interest

About the No Profit Rule:

Prevents a fiduciary from profiting personally from their fiduciary position beyond their agreed-upon compensation (and this is best achieved when the compensation is agreed-upon in advance of any specific recommendations, and the recommendation undertaken does not change the amount of the compensation)

Prohibits the fiduciary from using their position to secure any unauthorized additional benefit

Requires the fiduciary to account for and disgorge any secret profits obtained through their position

Applies even if the client suffers no actual loss

This is not to say that investment advisers and financial planners should not be compensated well. Those who have achieved true expertise and apply same for the benefit of their clients should be highly compensated as professional, trusted advisers. But compensation arrangements that result in differential compensation should be avoided, and in all instances the compensation received should not be unreasonable.

In summary.

A fiduciary relationship imposes duties of due care, loyalty and good faith on the fiduciary, who is to act only for the benefit of the client to the exclusion of all others (including the fiduciary and her or his firm).

Let’s face it – the fiduciary standard is tough. It is often characterized as the highest standard of conduct under the law.

If, as a profession, we are to move forward, then investment advisers and financial planners who are subject to the fiduciary standard must … must … must … fully understand the depth and breadth of the fiduciary duty of loyalty. And then must take actions to completely adhere to that standard – by avoiding conflicts of interest whenever possible.

Once we do this – and the regulators adopt rules that make it clear to consumers as to who is a true fiduciary, and who is a product salesperson – then an ever-greater number of consumers will trust fiduciary financial advisors, and the demand for financial planning and investment advice will soar.

Be a true, bona fide fiduciary. Take the high road. Structure your own practice to avoid conflicts of interest, wherever possible. Live a life of integrity and enjoy the rewards that come from possessing the trust of others and always acting for their benefit.

The foregoing represents the views of Ron A. Rhoades, JD, CFP(r), and are not necessarily representative of any firm, institution, or organization with whom he is or has been associated with, nor are they the views of any cult, gang, or motley crew that he has ever been kicked out from.

The 6% commission, a stardard in home purchase transactions, is no more.

In a sweeping move expected to dramatically reduce the cost of buying and selling a home, the National Association of Realtors announced Friday a settlement with groups of homesellers, agreeing to end landmark antitrust lawsuits by paying $418 million in damages and eliminating rules on commissions.

For our third episode of year six of the podcast, we welcome Herb Greenberg to the Investors First Podcast. Herb’s career is incredible, with time as a journalist at major news outlets ranging from the Chicago Tribune and San Francisco Chronicle, to the WSJ, and also time at The Street and CNBC. It should be noted that he was born and raised in Florida and attended the University of Miami. Herb’s energy and curiosity are up there with anyone we have interviewed in the history of this podcast.

In today’s episode, we cover a wide range of topics, starting with Herb’s successful career as a journalist, how he developed a niche in covering red flags on individual companies, how to use his intel to help mitigate risk, and what are his top red flags today, along with much more.

Today’s hosts are Steve Curley, CFA (Founder/Co-Managing Principal, 55 North Private Wealth) & co-host Chris Cannon (CIO/Principal, FirsTrust)

Scotty and Caroline didn’t inherit their wealth. They created it over a lifetime of hard work, diligent savings and prudent investing. And within the disciplined lifestyle that created it, they expect to pass a significant estate to their grandchildren after moderate consumption throughout their golden years.

Tax efficiency was a natural conversation starter as we engaged in their first estate planning discussions; both federal and state. As their assets pass into the next generation, their preference is to prudently disperse the funds over a period of time instead of all at once. And quite importantly, Scotty and Caroline intend for the funds to be used in a manner that makes a difference; one that instills values, inspires evangelical behaviors and rewards selflessness.

After a bit of research and discussion, my New York friends perceived their first step was to consult with a local estate planning attorney to create a NY trust. So, they were a bit surprised when I said, “Why a New York trust? A trust is an instrument of state law, each state’s laws are different, and you are free to choose which ‘situs’ is best for you!”

“Situs” establishes the essential, legal framework of the trust; all possibilities, and limitations, exist within that framework. And, as time passes and laws change as they often do, a properly drafted trust empowers the Trustee to shop for a more favorable situs as facts and circumstances surrounding the beneficiaries’ best interests emerge.

So, let’s go situs shopping.

Federal Estate Taxes

Among the few consistencies in estate planning is the impact that contemporary politics seems to have on the relevance of federal estate tax conversations. When I first entered the industry 38 years ago, each American taxpayer had a $192,800 tax credit, sufficient for exempting $600,000 of federal estate taxes. Today, in the first 100 days of the second Trump Administration, that exemption equivalent sits at about $28 million per married couple.

This federal tax regime presents an optimal and potentially brief planning environment – until next year. The future of the exemption hangs very much in the balance of the 119th Congress, and assuming no action, it will expire along with many components of 2017 Tax Cuts and Jobs Act.

Traditional trusts utilize this tax exemption for the benefit of both spouses over their lifetimes and thereafter disburse the funds to their children and grandchildren. Unfortunately, this simply kicks the can down the road to the next generation where the assets are – again – subject to taxes and creditors in the beneficiaries’ estates.

A “Dynasty Trust” created today can capture the existing $28 million exemption so it will always apply to the trust’s assets, along with all of its future growth, and provide for multiple generations of Scotty and Caroline’s children, grandchildren, and even great great-grandchildren, regardless of future political climates.

In Alaska, Idaho, New Jersey, Pennsylvania, Kentucky, Rhode Island, and South Dakota, the common law ”Rule Against Perpetuities” has been modified such that a Dynasty Trust can exist perpetually without ever being included in the beneficiary’s estate.

State Taxes

Closer to home for Scotty and Caroline lies the infamous web of New York state taxes (state income tax of 4%-10.9%, a city income tax of 3.078%-3.876%, a sales tax of 4% 8.875%, a property tax of about 1.64%, and a gas tax of about 25.68 cents). For half a century, NY even claimed tax authority over non-residents who had relocated to other states. (A lingering element of British common law that survived until only 25 years ago.) Scotty and Caroline’s legacy bequests include living expenses, college funds, and a very structured devise of purposeful stewardship for children and grandchildren. Income taxes, especially on an estate, are a dollar-for-dollar deterioration of these noble intentions. A Dynasty Trust created in Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming can avoiding the continued deterioration of New York taxes. There are also eight jurisdictions that do not impose their own state income tax on non-resident grantors and beneficiaries of Dynasty Trusts: Connecticut, Delaware, Georgia, Illinois, New Hampshire, Ohio, Tennessee and Wisconsin.

Stewardship

Well-informed consumers recognize the impact that money can have on their children and grandchildren, even as they become adults. Though Scotty and Caroline have no desire to “control from the grave”, they have both engaged in a lifetime of community stewardship and fully intend to endow successive generations with similar values and priorities. A Dynasty Trust can be fully customized to govern distributions in accordance with Scotty and Caroline’s specified purposes. It can condition distributions upon a beneficiary’s charitable endeavors or services, it can incentivize certain behaviors or educational achievements, and/or it can provide funds upon the Trustee’s discretion based upon the circumstances of the beneficiaries. Nevada, South Dakota, Delaware, Alaska and Wyoming are generally recognized among states with the most favorable flexibility in its laws and regulations.

Wealth Preservation

“Squander” is a rather pejorative reference to an unwise and rapid loss of windfall funds; commonly associated with lottery winners and trust fund spendthrifts. And even while the financial integrity of Scotty and Caroline’s heirs is not directly in doubt, it’s the rest of the world they should wisely question; the proverbial distant relative who suddenly appears seeking a “loan”, the opportunistic fortune hunters, the unscrupulously frivolous litigants, and unfortunately the surprise divorcee. A Dynasty Trust offers legal protections against these evils. When trust beneficiaries only receive funds at the discretion of the trustee, as Scotty and Caroline provide in the document, the assets are protected from frivolous litigation, divorcing spouses and even legitimate creditors of the beneficiary. Nevada, Ohio and South Dakota have recently exhibited a solid history of protecting trust assets.

Flexibility Dynasty Trusts are most often “irrevocable”. Today, however, that does not mean it can’t be changed. A legal process called “decanting” allows a trustee, acting in Scotty and Caroline’s interests and intentions, to move assets from an existing irrevocable Dynasty Trust to a new one with modified terms, essentially enabling future changes to the original trust without technically revoking it. While Alabama, California and Georgia have adopted a Uniform Trust Decanting Act, more flexible decanting provisions and trust modification options may exist in Nevada, South Dakota, Delaware, Alaska and Wyoming.

The Devil is In the Details

This is not an off-the-shelf trust. It requires advanced legal expertise, time and of course a bit of money.

The first Devil is in selecting the state jurisdiction that best accommodates Scotty and Caroline’s objectives. In my own professional experience, I’ve helped clients establish such domestic trusts when their specific priorities were best supported by the laws of Florida, Delaware, Alaska, and South Dakota; and other clients whose deeper objectives required a foreign, non-US (offshore) jurisdiction.

The second Devil is satisfying the various legal requirements for crafting a trust in their chosen state with the proper Trustee situs and asset nexus requirements that eliminate any possible ties back to their home state of New York.

The third Devil is the Corporate Trustee, which should be categorically avoided. Scotty and Caroline should consider a qualified Independent Trustee or Independent Trust company who won’t charge excessive fees, stray from their stated directives, or attempt to rationalize the conflict of interest that accompanies serving as both Trustee and investment manager.

It’s my opinion that the perfect storm exists today for Scotty and Caroline to successfully avoid taxes, protect their wealth, and achieve their stewardship objectives for many generations beyond them.

Author: Mike Koenig, Founding Partner of FirsTrust, LLC, candidly and unapologetically shares his 36 years of experience as a financial advisor to advocate truth and transparency for financial service consumers. His education and experience includes a bachelor’s degree in psychology from the University of Maryland, a master’s certificate in finance from George Washington University, a Juris Master of Law degree from Florida State University College of Law, and the CFP® Certified Financial Planner™ professional designation

800-585-9888

800-585-9888

“Situs” establishes the essential, legal framework of the trust; all possibilities, and limitations, exist within that framework. And, as time passes and laws change as they often do, a properly drafted trust empowers the Trustee to shop for a more favorable situs as facts and circumstances surrounding the beneficiaries’ best interests emerge.

“Situs” establishes the essential, legal framework of the trust; all possibilities, and limitations, exist within that framework. And, as time passes and laws change as they often do, a properly drafted trust empowers the Trustee to shop for a more favorable situs as facts and circumstances surrounding the beneficiaries’ best interests emerge.